There are various business models that operate in retail wealth management, some firms offer a specific business model whereas other firms operate on multiple business models giving the customers the flexibility to choose the business model that suits best to their needs.

| No model is likely to dominate the global wealth management because they are designed around different target customers |

Primarily there are three main types of business models – Universal banks, Platform players and Private Banks and Brokerages. Various Broker affiliated advisors, RIA (Fee-based business), Hybrid and Dual registration, Robo Advisors etc. use full-service firms, Banks, Independent broker-dealers, Self-directing firms, self-clearing firms, discount brokerages, global financial firms etc. some of these business models are explained in details below.

The Business models differ from country to country and the challenges of different business models are similar. It is a difference in the regulatory regimes of the country. The customization of their services for the national markets and selection of products based on the maturity of the maturity of markets

Key Players

Traditionally, the industry was dominated by private banks and stockbrokers. But there were important regional differences in the dominant types of player. To some extent, this reflected differences in the structure and regulation of the financial services industry as a whole. Broadly, there are two main models:

- North American model, where the industry is dominated by full-service and discount brokerages and money managers, whose strengths lie in the investment area, rather than in traditional deposit gathering, as noted above, the traditional emphasis here is on a (transaction driven) commission-based business model.

- The European model, where universal and traditional private banks dominate, due to their ability to offer a comprehensive range of wealth management products and services. The emphasis here is on a fee-based business model.

Registered Investment Advisors (RIA)

These investment advisors (IA) are registered with SEC under the Investment adviser’s act of 1940 in the USA. An IA must adhere to a fiduciary standard of care laid out in the US Investment Advisers Act of 1940. This standard requires IAs to act and serve a client’s best interests with the intent to eliminate, or at least to expose, all potential conflicts of interest which might incline an investment adviser—consciously or unconsciously—to render advice which was not in the best interest of the IA’s clients . It is one of the fastest-growing sectors, benefiting from advisor and asset migration away from wirehouses. Strong client relationships, supported by product and operational support from large-scale platform providers.

The vast majority of broker-dealer firms serving retail clients also operate a separate RIA firm, which we refer to as a corporate RIA. The assets managed by corporate RIAs are not included in the independent RIA subsegment; rather, assets managed under a corporate RIA structure are rolled up under each broker-dealer firm’s subsegment. Representative firms in the independent RIA subsegment include Oxford Financial Group, Shepherd Kaplan, and Appleton Partners.

Digital advisors/Robo-Advisors

Over recent years, a number of web-based advisors have emerged. They offer above-average advisory quality and act as a gateway to third-party product providers. They are Innovative providers leveraging technology, social media, and communities to attract younger and self-directed investors Data aggregation is a key value proposition of this new breed of Financial Advisors.

Family offices

They serve the very wealthiest clients, acting as an integrated hub for the family’s financial administration. They perform, essentially, three main functions:

- Specialist advise and planning (including financial, tax, strategic and philanthropic);

- Investment management (including asset allocation, risk management, investment due diligence and analysis, discretionary asset management and trading); and

- Administration (including coordination of relationships with financial services providers and consolidated financial reporting).

A family office may be dedicated either to a single family or serve a small number of families. Some of the major private banks, such as Pictet and JP Morgan, have developed their own multifamily offices, but the vast majority are independent specialists (and have, in some instances, evolved from single family offices). Family offices are particularly well-developed in the US and are starting to evolve in Europe

Private Banks

Is a broad category of players that includes the classic Swiss private banking partnership, mainly targeting HNWIs, these institutions offer clients end-to-end capabilities via a relationship with a senior banker (the relationship manager) that is confidential and founded on trust.

Retail and universal banks

They target affluent clients who need comprehensive advice and who value a close banking relationship and the emphasis is on ‘farming’ their existing customer base, including business banking clients. Examples include Citigroup, HSBC, Bank of America.

Trust banks

Are essentially the US equivalent of the traditional European private bank. Most have their roots in providing trust and custody services but have broadened their product range over the years. They now also provide asset management, insurance and financial, tax and estate planning. Their core target client segment is UHNWIs, but many have also developed tailored propositions for HNWIs

Stockbrokers and Wirehouses

Target self-directed investors and traders for their day-to-day transaction execution and investment needs, they offer low-cost access to a range of investment products as well as to extensive investment research. But they are not exclusively dedicated to affluent clients, do not typically offer much in the way of customized advice and often lack transaction banking products. It is a diverse group, including firms that have their roots in online discount brokering such as E*TRADE, as well as full-service brokers such as Morgan Stanley.

Product specialists

Include hedge funds, private equity funds, mutual funds and structured product providers. Lacking their own captive distribution channels, they manufacture products for distribution across a range of HNW channels, including private banks and financial advisors

Self-clearing retail brokerage (non-Wirehouses)

It refers to a group of large to mid-size national and regional broker-dealer firms (excluding the aforementioned Wirehouses) those clear securities transactions for themselves. Representative firms in this sub-segment include Edward Jones, Ameriprise, RBC Wealth Management, and Raymond James.

Fully disclosed retail brokerage

This refers to all broker-dealer firms that utilize another broker-dealer to clear securities transactions on their behalf (with the exception of some fully disclosed discount and online brokers, which are included in the discount and online brokerage subsegment). Fully disclosed broker-dealers are also referred to as introducing broker-dealer firms. Sample firms in this subsegment include Commonwealth Financial Network, First Allied Securities, and NFP Securities.

Discount and online brokerage

This subsegment refers to broker-dealer firms that cater to self-directed investors by offering low-cost securities execution. The majority of firms in this subsegment engage with clients via a Website. Representative firms in this segment include divisions of Fidelity, Charles Schwab, and TD Ameritrade.

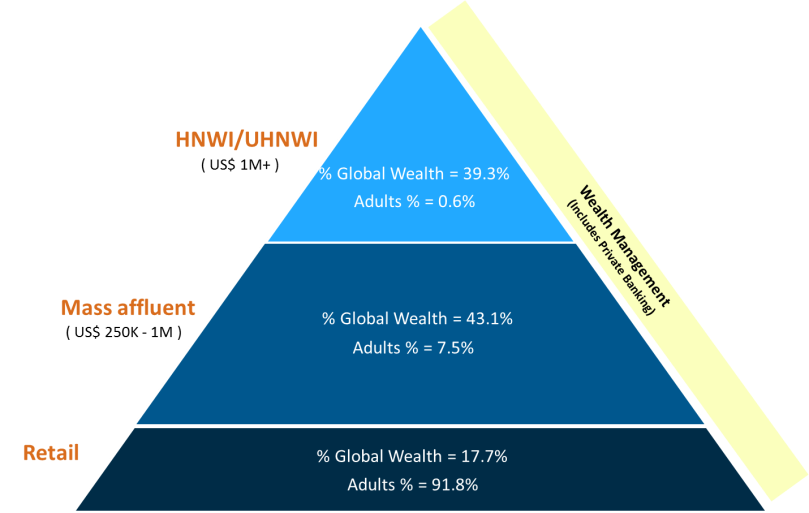

Investor Categorization

Wealth management clients are changing and they are growing in number and in complexity and based on the global financial assets they have been categorized as HNW/UHNW, Mass affluent and Retail customer. In order to categorize the customer net worth, the assets like cash and deposit, equity and bonds, mutual funds, alternative investments and IRA are considered. Some of the assets like the residential real estate, occupational pension assets and household debt are not considered.